Annuities, as financial products, are often misunderstood but can play a vital role in a robust retirement strategy. As individuals approach retirement, the need for guaranteed income becomes paramount, leading many to consider annuities as a solution. This article aims to explore what annuities are, how they function, their advantages and disadvantages, the different types available, and how they compare to other investment options.

Additionally, understanding the nuances of annuities can empower you to make informed decisions about your financial future. By breaking down their benefits and drawbacks, this article will help clarify whether annuities suit your personal financial situation and retirement plans. If you're contemplating purchasing an annuity or simply want to learn more about these financial products, keep reading to find out more.

Ultimately, becoming educated about annuities can help you craft a financial strategy that aligns with your goals, ensuring you have the means to enjoy your retirement years without financial stress. Thus, a thoughtful examination of both the pros and cons is necessary.

What are Annuities?

An annuity represents a financial product sold by financial institutions that provide a steady stream of income over time, often utilized for retirement purposes. At its core, an annuity is a contract between you and an insurance company where you make a lump sum payment or a series of payments in exchange for periodic disbursements in the future.

The primary goal of an annuity is to accumulate funds for retirement or other long-term targets, ensuring that you do not outlive your savings. They offer a unique blend of investment and insurance features, making them stand apart from typical investment options.

There are numerous types of annuities available, each suited for different financial needs and objectives. This flexibility allows individuals to design a retirement strategy that aligns with their lifestyle and income needs.

How Annuities Work

Annuities work through a two-phase process: the accumulation phase and the distribution phase. In the accumulation phase, you pay into the annuity, either as a lump sum or through a series of payments. Over time, your investment grows, often on a tax-deferred basis. This means you won't pay taxes on any earnings until you begin to withdraw funds.

In the distribution phase, the annuity pays out returns, which could be in the form of regular payments for a predetermined period or for the rest of your life. The structure of these payments can vary, offering a level of flexibility important for retirement planning.

The amount you receive during the distribution phase is determined by several factors, including the type of annuity, the length of the payment period, and your age at the time of annuitization.

- Annuities can be structured in numerous ways to cater to different financial objectives and risk tolerances.

- They often include options for death benefits, ensuring beneficiaries receive funds after the annuitant's passing.

- Annuities may be fixed or variable, influencing how much income you receive and the associated risks.

- Some annuities offer growth potential tied to market performance, allowing for a possibly higher return.

Understanding the mechanics of how annuities function is crucial for anyone considering them as a financial tool. With this knowledge, individuals can make informed choices about whether to incorporate annuities into their retirement planning.

Pros of Annuities

One of the foremost benefits of annuities is the provision of guaranteed income during retirement, regardless of market volatility. This feature creates a sense of financial stability, important for most retirees who fear outliving their savings due to unforeseen expenses or extending life expectancy.

Furthermore, many annuities offer added benefits like tax deferral on earnings, which can enhance the growth of your investment over time. This can be advantageous for retirees seeking to maximize their retirement savings before drawing on them.

- Guaranteed income stream for life, reducing the risk of outliving your assets.

- Tax-deferred growth of investment, leading to potentially higher accumulations over time.

- Customizable features, including options for beneficiaries and riders that maximize benefits.

- Protection from market downturns, as fixed annuities provide stable returns regardless of economic conditions.

These advantages make annuities an appealing option for many planning their financial futures, particularly for those prioritizing stability and income predictability in retirement.

Cons of Annuities

Despite their advantages, annuities come with several disadvantages that potential buyers should consider. For starters, they often involve complicated contracts with various fees and penalties that can eat into your investment growth and returns. Understanding these costs is crucial before entering into an agreement.

Moreover, once funds are invested in an annuity, withdrawal penalties can be steep if you decide to access your money early, which limits liquidity and can create challenges in emergencies.

- High fees that can diminish your overall returns.

- Penalties for early withdrawal before a contract's terms are met.

- Limited access to capital, reducing liquidity.

- Complex contracts that require thorough understanding.

These cons underscore the importance of conducting careful research and possibly consulting with a financial advisor to ensure that an annuity aligns with your overall financial strategy.

Types of Annuities

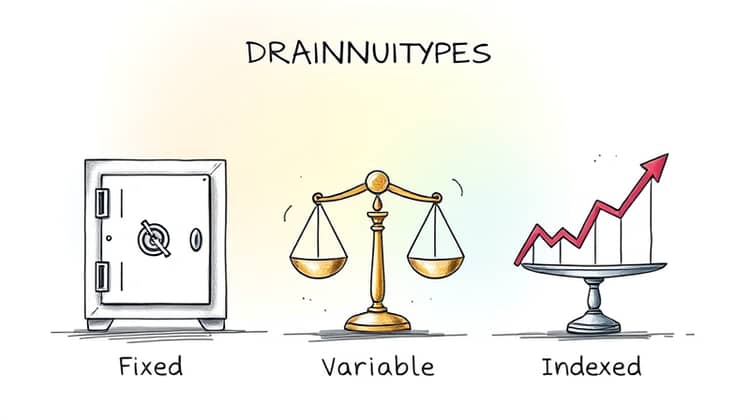

Annuities can be categorized into several types, each varying in structure and intended purpose. For instance, fixed annuities provide a guaranteed return on your investment and predictable payment amounts, making them a conservative choice for risk-averse individuals. In contrast, variable annuities allow for investment in different assets, which can lead to higher returns, but also come with increased risk.

Another category includes indexed annuities, which tie returns to a stock market index and offer potential for higher earnings while providing some degree of principal protection. Understanding the different types can help in selecting the one that best meets your needs.

- Fixed Annuities - offer guaranteed returns and fixed payments.

- Variable Annuities - allow investment in various options with variable returns.

- Indexed Annuities - linked to a specific index providing potential higher returns with some protections.

Choosing the right type of annuity is essential for achieving your financial objectives, so consider your risk tolerance, investment strategy, and retirement goals carefully before making a decision.

Annuities vs. Other Investment Options

When comparing annuities to other investment options, several key distinctions emerge. Unlike traditional stocks and bonds, which can be subject to market volatility, annuities usually provide guaranteed returns or income. This makes them a unique alternative for those focusing on retirement income.

However, while annuities offer stability, they may lack the growth potential that often comes with direct stock market investments. Additionally, the tax implications differ, as annuities grow tax-deferred, while traditional investments may incur capital gains taxes when sold.

Conclusion

In summary, annuities offer a unique fusion of security and income potential, making them a compelling option for many contemplating their retirement strategies. Their ability to provide guaranteed income can alleviate concerns about financial stability during retirement, but it's essential to navigate the complexities and costs associated with these products.

Ultimately, by thoroughly understanding annuities, their advantages and disadvantages, and how they fit into the broader investment landscape, individuals can make well-informed decisions that enhance their financial security in the years to come.