Credit cards can offer convenience and flexibility, but they can also lead to financial strain, especially if you encounter unexpected expenses. Many people find themselves struggling to meet payment deadlines and accumulating debt. In these challenging times, credit card hardship programs can provide critical relief.

These programs are designed for individuals facing financial hardships, offering options such as reduced payments, lower interest rates, or even debt forgiveness. Understanding the timeline for enrollment and the specific benefits can be key to managing your financial situation effectively.

In this article, we will explore when to consider a hardship program, what these programs can offer, their potential downsides, and how to enroll in one. Additionally, we'll discuss other options available for those in financial distress.

When Should You Consider a Hardship Program?

A credit card hardship program may be a viable option when you find it increasingly difficult to make your monthly payments due to circumstances such as job loss, medical emergencies, or other unforeseen financial burdens. Recognizing the early signs of financial trouble is crucial; this could include falling behind on payments, receiving collection calls, or using credit to make essential purchases.

It is important to evaluate your overall financial situation before enrolling in a hardship program. Analyzing your income, necessary expenses, and existing debts can provide clarity on whether a hardship program is the right choice for you. If you find that your financial challenges are temporary, a hardship program can offer immediate relief while you work toward a long-term solution.

Consider the benefits of a hardship program compared to simply missing payments or defaulting on your credit card. A formal hardship program may help you negotiate better terms with your creditors and prevent damage to your credit score.

Ultimately, if your ability to pay is compromised and you have already attempted to manage your debts through other means, it may be time to explore hardship options.

What Do Hardship Programs Offer?

Hardship programs typically provide a range of benefits aimed at alleviating financial stress for cardholders. The specifics of these programs can vary by lender, but most offer similarities in terms of what they provide to help consumers.

Common offerings include reduced monthly payments, lower interest rates for a period, or even deferred payments without penalties. Some programs might also negotiate a settlement on your outstanding balance.

- Reduced monthly payments that are easier to manage.

- Lower interest rates or temporary waivers on fees.

- The possibility of deferred payments for a specified time.

- Potential for debt forgiveness or settlements in extreme cases.

These measures help you navigate through temporary financial difficulties without incurring further debt, allowing some breathing room to stabilize your circumstances.

What Are the Downsides?

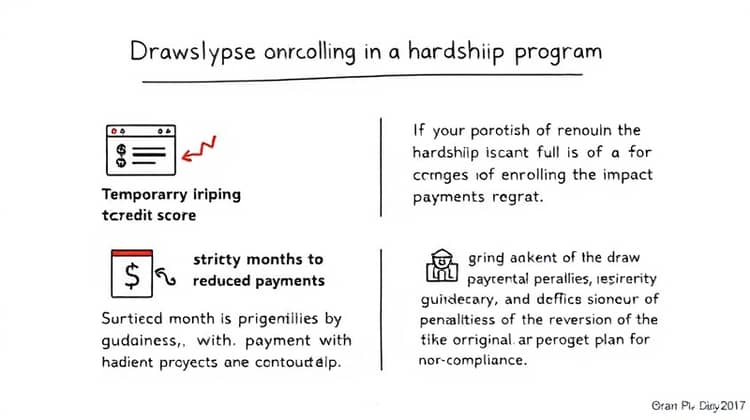

While hardship programs can offer critical assistance, there are potential downsides to carefully consider. For instance, enrolling in a hardship program may negatively impact your credit score temporarily. Creditors often report your participation in a hardship program to the credit bureaus, which can affect your ability to secure new credit or loans.

Furthermore, some hardship programs may have specific terms that require adherence to certain guidelines, such as multiple months of reduced payments and not accruing additional debt during this period. Failure to comply with these terms could result in the reversion of your original payment plan or even lead to further penalties.

Lastly, some lenders may view your need for a hardship program as a risk factor, which could affect future lending decisions and your overall creditworthiness.

- Potential negative impact on your credit score.

- Strict adherence to program terms that may limit financial flexibility.

- Lenders may view participation as a red flag for future credit approvals.

Understanding these drawbacks is essential for making a fully informed decision regarding whether to enroll in a hardship program.

How to Sign Up for a Credit Card Hardship Program

If you've decided that a hardship program is the right option for you, the next step is to reach out to your credit card issuer to discuss eligibility and the application process. Most creditors will require you to provide documentation related to your financial situation, such as income statements or bills that illustrate your hardship.

It is crucial to be honest and thorough when explaining your financial challenges. Some lenders may also provide forms to fill out, detailing your income, expenses, and any other debts you may have.

- Contact your credit card issuer directly via phone or their customer service portal.

- Gather necessary documentation (income statements, bills for proof).

- Explain your hardship situation clearly and ask about available programs.

- Inquire about the specific terms and conditions of the hardship program.

Once enrolled, be sure to keep clear communication with your issuer and understand the terms of your agreement to avoid any pitfalls that may arise during the program duration.

Other Options Besides Signing Up for a Hardship Program

If a hardship program does not seem suitable for your circumstances, there are other avenues you can explore. For instance, negotiating directly with your creditor can sometimes yield favorable payment terms without formally enrolling in a hardship program.

Additionally, consolidating your debt through a personal loan can provide lower interest rates, helping you make one manageable monthly payment rather than multiple credit card payments.

- Negotiate directly with creditors for temporary relief.

- Consider debt consolidation options with lower interest rates.

- Explore credit counseling services for debt management advice.

- Look into budgeting and financial planning support.

Assessing these alternatives thoroughly could provide you with tools to manage your debt without the long-term commitments associated with hardship programs.

Conclusion

In summary, credit card hardship programs can offer essential relief during tough financial times, providing options to manage or alleviate debt burdens. However, it is crucial to weigh the potential downsides along with the program benefits to determine whether it aligns with your individual financial situation.

If you find yourself in a financial crisis, exploring hardship programs or alternative solutions can help you regain control of your financial health, allowing you to move forward more positively. Make sure to stay informed about the options available, and always communicate openly with your creditors.