Retention offers are a key strategy credit card companies use to retain customers who may be considering canceling their cards. These offers can include bonuses, discounts on fees, or increased points on purchases, enticing customers to stay loyal to the issuer.

To successfully receive a retention offer, understanding how they work and the specific timing and strategies involved is essential. This article will delve into everything you need to know about credit card retention offers, including how to ask for them and whether they are worth pursuing.

How Retention Offers Work

Credit card retention offers are incentives provided by credit card issuers to keep customers from closing their accounts. When a cardholder expresses the intent to cancel their card, customer service representatives may present various offers to dissuade them from doing so. These offers are often tailored to the customer's spending habits and history with the credit card.

The goal of these retention offers is to maintain the cardholder's business, as acquiring new customers can be significantly more expensive for companies than retaining existing ones. This dynamic creates opportunities for consumers to negotiate and potentially secure benefits that enhance the value of their credit cards.

Which Credit Cards Offer Retention Value?

Many credit cards come with the potential for retention offers, particularly premium cards that carry higher annual fees. Cards from major issuers such as Chase, American Express, Citibank, and Bank of America often provide these offers as a part of their customer service strategy.

Specific cards may vary in the types of offers they present, but popular rewards cards frequently entice loyalty through retention offers, particularly when cardholders have been long-standing customers or have substantial accrued rewards. This provides leverage for negotiation when considering retention offers.

- Chase Sapphire Preferred

- American Express Gold Card

- Citi Premier Card

- Bank of America Premium Rewards Card

These cards are well-known for offering significant value, and retention offers can further enhance this by providing additional perks or rewards that can make the cards more appealing to hold on to.

When Is the Best Time to Ask for Retention Offers?

The best time to ask for retention offers is typically right after receiving your annual fee statement or when you are considering switching to another card due to better rewards or benefits. This timeframe allows you to express your dissatisfaction with the current offer and leverage that to ask for a retention offer.

Additionally, if you notice that you aren’t maximizing the benefits of your current card, it’s a good opportunity to evaluate if there are retention offers that could enhance your experience and provide additional value.

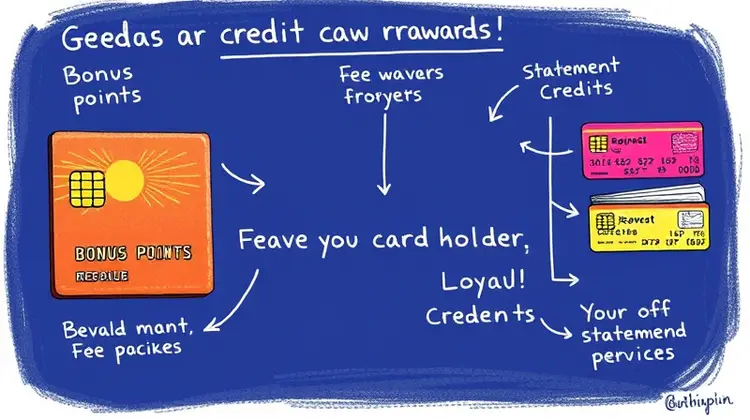

What Kind of Retention Offers Will You Receive?

Retention offers can take various forms, each aimed at either increasing your rewards, reducing your fees, or enhancing your cardholder experience. Common types include bonus points for staying, waiving the annual fee, or providing statement credits. These offers are often temporary and can be influenced by your previous spending habits and loyalty to the card issuer.

The exact offerings will depend on the card network and how valuable your account is deemed based on your activity and payment history, leading to a personalized retention offer that seeks to maximize your satisfaction with the card.

Strategies to Use When Asking for a Retention Offer

When approaching your credit card issuer for a retention offer, it’s crucial to be prepared with information and a clear understanding of what you are seeking. Being respectful and patient during the conversation can go a long way in facilitating a favorable outcome.

- Research your card's typical retention offers.

- Be honest about your reason for considering cancellation.

- Mention competitor offers you have received.

- Highlight your loyalty and good standing with the card.

Employing these strategies increases your chances of receiving a favorable retention offer, making it more likely that the card issuer sees you as valuable and worth keeping as a customer.

How to Ask for a Retention Offer

To ask for a retention offer effectively, start by calling your card issuer's customer service number. Once connected, express your intention to cancel your card while being clear and concise about your reasons. It’s important to remain polite and professional, as the representative is there to help you.

Next, be prepared to share specific examples of why you feel the card does not meet your needs and mention any competitor cards that offer better terms. This not only sets the stage for negotiation but also shows that you are informed and serious about your decision.

Finally, after laying the groundwork, directly ask if any retention offers are available to you as a loyal customer. This clear request often prompts the representative to present various options and helps facilitate a productive dialogue.

- Call the customer service number of your credit card issuer.

- Express your desire to cancel the card and state your reasons.

- Ask directly for any available retention offers.

Following these steps can help in not only securing a retention offer but also ensuring that the experience remains positive, leading to an outcome that benefits both you and the issuer. It’s all about open communication and negotiation when done correctly.

Are Retention Offers Worth It?

Retention offers can be quite valuable, especially if you are considering canceling a card with high annual fees or limited rewards. Evaluating the offers received can provide additional benefits which might outweigh the costs associated with keeping the card, helping you make a more informed decision.

Additionally, if the retention offer includes options to earn bonus points or cash back that align with your spending habits, they can significantly enhance the value of your membership, leading to much more attractive terms than possibly switching to a new card altogether.