Debt is a reality for many Americans, with millions struggling to keep up with multiple payments across various credit accounts. Debt consolidation loans present a possible solution for those looking to streamline their finances by combining all their debts into a single loan. While it can seem like a lifeline, it's important to understand the pros and cons associated with debt consolidation loans before making any decisions.

In this article, we'll dive into what debt consolidation loans are, how they operate, their benefits and drawbacks, different types available, and how to apply for one. We’ll also help you assess whether debt consolidation is the right choice for your financial situation or if alternative solutions may suit you better.

By the end of this article, you'll have a better grasp of what debt consolidation entails and how it can impact your financial health, setting the stage for informed decision-making.

What is Debt Consolidation Loan?

A debt consolidation loan is a financial strategy used to combine multiple debts into a single loan, typically featuring a lower interest rate than the existing debts. The primary purpose of using a debt consolidation loan is to simplify payments and potentially save on interest costs.

Instead of making several monthly payments to different creditors, the borrower makes just one payment each month to the debt consolidation lender. This can make managing finances simpler and may free up cash flow that can be redirected towards savings or other obligations.

Debt consolidation can involve personal loans, balance transfer credit cards, or home equity loans, among other options. While this approach can be effective for some borrowers, it’s crucial to understand the details and implications before proceeding.

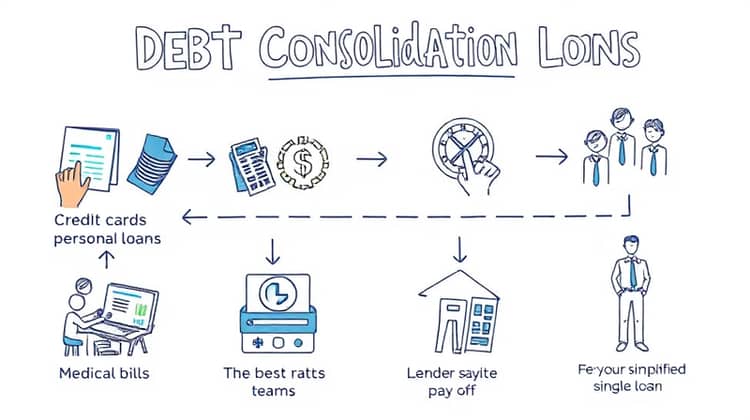

How Do Debt Consolidation Loans Work?

Debt consolidation loans work by using one loan to pay off multiple debts, allowing you to consolidate what you owe into one monthly payment. To start the process, borrowers typically assess their total debt and identify how much they owe across various accounts, such as credit cards, personal loans, or medical bills.

Once you have a total amount, you can look for lenders that offer debt consolidation loans with favorable terms—such as lower interest rates and long repayment periods. After comparing rates and terms, you choose the lender that best fits your financial situation.

When you receive the loan, the lender pays off your existing debts directly, and you’re left with a single loan for the new amount. This simplifies your monthly payments and can even lower your overall debt payments if your new loan's interest rate is lower than the rates of your previous debts.

It's critical to remember that the success of debt consolidation largely depends on your ability to manage finances responsibly going forward, as simply consolidating debt without a change in spending habits can lead to accumulating more debt.

The Benefits of Debt Consolidation Loans

One of the primary benefits of debt consolidation loans is the simplification of multiple payments into one monthly payment. This approach helps borrowers manage their finances better and can reduce the likelihood of missed payments, which can lead to additional penalties and damage to credit scores.

Additionally, many users find that a new consolidation loan can lower their interest rates compared to their existing debts, leading to potential savings on monthly payments and the total interest paid over the life of the loan. By decreasing the cost of borrowing, debt consolidation can help propel individuals closer to becoming debt-free.

Moreover, debt consolidation loans provide a structured repayment schedule that can often be easier to manage than the varied due dates and payments for multiple creditors. Having a fixed term allows borrowers to strategize their finances more effectively. Most importantly, it empowers borrowers to take control of their debts and invest in their financial well-being.

- Simplified payments with one monthly payment

- Potentially lower interest rates compared to existing debts

- Structured repayment schedule for better financial management

Considering the benefits, debt consolidation can be a powerful tool for those struggling with multiple debts, but it’s essential to weigh the pros against the potential drawbacks.

The Drawbacks of Debt Consolidation Loans

Despite the advantages, debt consolidation loans come with their share of drawbacks. Some borrowers may find they don’t qualify for better interest rates, especially if they have poor credit or high debt-to-income ratios. If the interest rates are not significantly lower than existing debts, the consolidation effort could be futile.

Moreover, consolidating debts may also prolong the repayment period, which could lead to paying more interest over time despite the lower monthly payments. It’s critical to understand the terms and conditions before committing, as some consolidation loans will take unsecured debts (like credit card debt) and turn them into secured loans, which could risk personal assets if payment obligations are not met.

- Possibility of not qualifying for lower interest rates

- Longer repayment periods can result in higher overall interest costs

These drawbacks highlight the need for careful consideration before opting for debt consolidation. Each individual's financial situation is unique, and weighing the potential risks against the motivations for consolidating debts can clarify the best path forward.

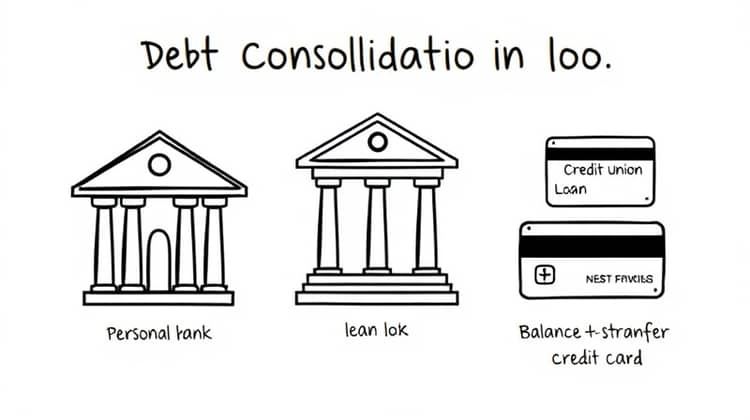

Types of Debt Consolidation Loans

Not all debt consolidation loans are created equal; there are several types available to borrowers depending on their needs and circumstances. One common type is a personal loan from a bank or credit union wherein a borrower takes out a lump sum to pay off existing debts, thus focusing on a single repayment. This is often a straightforward method for borrowers with good credit.

Another popular option is a balance transfer credit card, which allows borrowers to transfer existing credit card balances to a new card with a lower interest rate. Many of these cards offer promotional 0% APR for a limited time, helping borrowers manage payments, although fees may apply for transferring balances.

- Personal loans from banks or credit unions

- Balance transfer credit cards with introductory 0% APR offers

- Home equity loans or lines of credit

Understanding the various types of debt consolidation loans can assist borrowers in choosing the option that best fits their financial needs and situation.

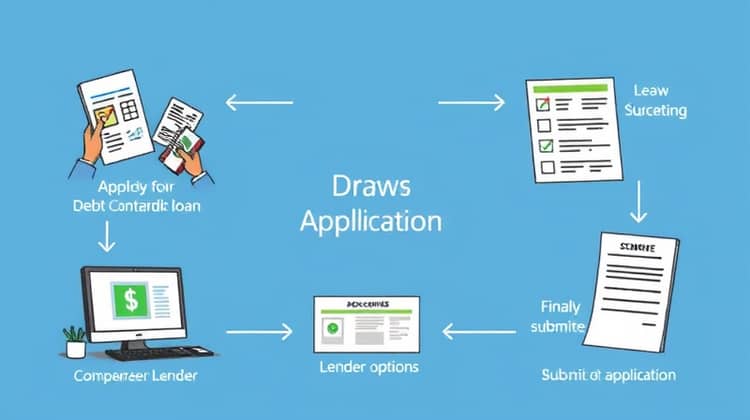

How to Apply for a Debt Consolidation Loan

Applying for a debt consolidation loan is similar to applying for any other loan. It typically involves gathering financial documents, assessing your credit score, and checking your debt-to-income ratio to understand your borrowing capacity.

- Evaluate your current debt situation and total amount owed.

- Check your credit score and credit report to understand your creditworthiness.

- Research and compare lenders to find favorable terms and interest rates.

- Submit your application along with the necessary documentation and await approval.

Once approved, you can use the funds to pay off your other debts and start your journey towards financial recovery.

Is Debt Consolidation Right for You?

Determining if debt consolidation is right for you depends on your financial situation, credit status, and long-term goals. If you have high-interest debts and a manageable credit score, consolidating into a single loan with a lower rate can be beneficial. However, if your financial issues are rooted in spending habits, it's crucial to address those habits alongside any consolidation efforts.

Conclusion

In conclusion, debt consolidation loans can provide a viable path to simplify debt management and potentially save money on interest. However, the appropriateness of this strategy depends on individual financial circumstances, including the type of debts, total owed, and credit status.

When considering debt consolidation, assess all available options thoroughly, and ensure you're aware of the terms and conditions of any loan products you're looking at. Remember to reflect on your financial behaviors to avoid accumulating debt again, as addressing root issues is essential for long-lasting improvement.

For many, debt consolidation can be an effective first step towards overcoming debt, but it must be approached with careful consideration and planning.