Home equity loans can be a valuable financial resource, allowing homeowners to access the wealth tied up in their properties. As home values increase, the equity you hold in your home can be harnessed for various needs—be it home renovations, debt consolidation, or education expenses. This article aims to shed light on how home equity loans function, their benefits, and their potential drawbacks to help you make informed decisions about accessing your home’s equity.

Understanding home equity loans is essential for homeowners considering leveraging their property’s value. They are distinct financial products that require careful consideration. This article breaks down everything you need to know, including eligibility requirements, the application process, and responsible usage. By the end, readers will gain a comprehensive insight into home equity loans and how they can fit into their financial strategy.

Whether you need a lump sum for a major purchase or an efficient way to finance renovations, home equity loans offer a range of solutions. Knowing how to navigate this financial tool will empower homeowners to unlock their home value effectively and responsibly. Let's dive in!

What is a Home Equity Loan?

A home equity loan is a type of financing that allows homeowners to borrow against the equity in their property. Equity is the difference between the market value of your home and the outstanding balance on your mortgage. Essentially, it represents the amount of your home that you truly own.

Home equity loans are often referred to as second mortgages because they are a lien on your home, just like your first mortgage. When you take out a home equity loan, you receive a lump sum amount that you can use for various purposes, with the agreement to repay the loan, along with interest, over a predetermined period.

These loans typically come with fixed interest rates, which means your monthly payments will remain steady throughout the life of the loan.

- Provides access to cash for emergencies, home improvements, or consolidating debt.

- Often has lower interest rates compared to credit cards or personal loans.

- The interest on a home equity loan may be tax-deductible, depending on the usage of funds.

Home equity loans provide a straightforward way to access funds, often with favorable terms. However, understanding the full implications of borrowing against your home is crucial.

How Do Home Equity Loans Work?

When you take out a home equity loan, lenders evaluate your property’s value and your remaining mortgage balance to determine your equity stake in the home. This assessment involves an appraisal of the property, which may require payment upfront.

Lenders generally allow you to borrow a percentage of your equity, often up to 85%, although this can vary based on individual circumstances and lender policies. This limit means you'll need to leave some equity in your home to protect the lender's investment and ensure you remain financially stable.

The loan amount you qualify for is determined by your creditworthiness, income, and the current market value of your home.

Types of Home Equity Loans

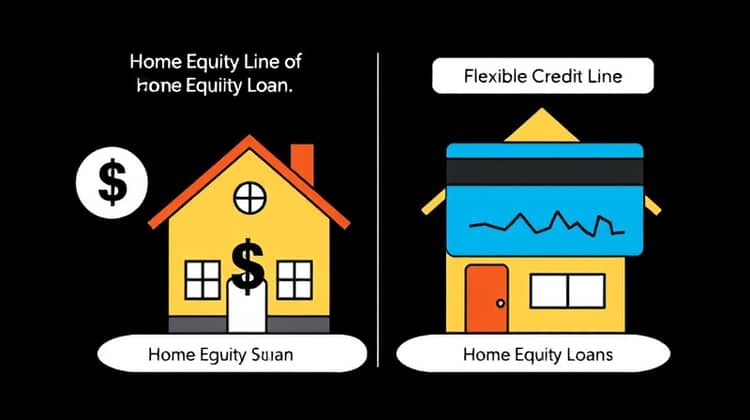

There are primarily two types of home equity loans—traditional home equity loans and home equity lines of credit (HELOCs). A traditional home equity loan provides a single lump sum amount to be paid back over a fixed term, while a HELOC allows homeowners to borrow against their equity as needed, similar to a credit card.

- Traditional Home Equity Loan: A fixed-rate loan for a lump sum.

- Home Equity Line of Credit (HELOC): A revolving credit line based on equity.

Choosing the right type of home equity option depends on your financial needs and borrowing habits.

Advantages of Home Equity Loans

Home equity loans offer several advantages that can make them an appealing option for homeowners. First, they often come with lower interest rates than unsecured loans, making them more affordable for borrowing larger sums of money. Additionally, the fixed interest rates provide predictable monthly payments, making budgeting easier.

Second, home equity loans can be a powerful tool for consolidating higher-interest debts, such as credit cards or personal loans, effectively lowering your overall monthly payments. This debt consolidation can significantly reduce the financial stress on a homeowner’s budget.

Finally, the potential for tax-deductible interest payments can make home equity loans even more advantageous, depending on how the borrowed funds are utilized.

- Lower interest rates than credit cards or personal loans.

- Fixed monthly payments make budgeting easier.

- Potential tax benefits on interest payments.

With these advantages in mind, many homeowners see the appeal of home equity loans as a way to tap into their property's value in a structured and manageable way.

Disadvantages of Home Equity Loans

While home equity loans offer numerous benefits, there are also potential pitfalls that borrowers should be aware of. One significant disadvantage is the risk associated with using your home as collateral. If you are unable to make your loan payments, the lender may foreclose on your home, leading to a loss of your property.

Additionally, taking out a home equity loan can lead to additional debt, which may strain your finances, especially if you borrow beyond your means or fail to adhere to a responsible repayment plan.

Finally, the costs associated with obtaining a home equity loan can add up, including closing costs and appraisal fees, which may make it less advantageous for some homeowners.

- Risk of foreclosure if unable to repay.

- Potential for increased overall debt burden.

- Closing costs and fees can add to the expense.

Recognizing these disadvantages is crucial for homeowners considering a home equity loan, emphasizing the importance of thorough planning and financial scrutiny.

Home Equity Loan vs. Home Equity Line of Credit (HELOC)

Home equity loans are oftentimes compared to home equity lines of credit (HELOCs), as they both allow homeowners access to their equity. However, there are fundamental differences between the two that can impact your choice of financing.

- A home equity loan provides a lump sum for immediate use, while a HELOC offers a flexible credit line you can draw from as needed.

- Home equity loans usually have a fixed interest rate, whereas HELOCs typically feature variable rates that can fluctuate with market changes.

- Repayment terms differ; home equity loans often start repayment immediately, while HELOCs usually have an initial draw period followed by a repayment period.

Understanding these differences can help homeowners choose the financing option that best fits their financial situation and future plans.

How to Qualify for a Home Equity Loan

To qualify for a home equity loan, lenders typically require that you have a good credit score, a stable income, and sufficient equity in your home. A credit score above 620 is generally preferred, but higher scores can lead to better interest rates and terms.

Lenders will also consider your debt-to-income (DTI) ratio to ensure you can manage the additional loan payments along with your existing obligations. This ratio measures how your total monthly debt compares to your gross monthly income, with a lower ratio indicating better financial health.

Finally, documentation regarding your income, asset holdings, and existing liabilities will be required to support your loan application.

- Maintain a good credit score (generally above 620).

- Demonstrate a stable income to cover loan payments and existing debts.

- Provide documentation of income and liabilities as part of the application process.

Meeting these requirements increases your chances of securing a home equity loan with favorable terms.

The Application Process

Applying for a home equity loan typically involves several stages, starting with research and selecting a lender that meets your needs. It's advisable to compare interest rates, fees, and terms from various lenders to find the best option.

Once you've chosen a lender, you'll need to complete an application, including providing relevant financial information and documenting your income. After your application is submitted, the lender will usually perform an appraisal of your home to determine its current market value.

- Research potential lenders and compare options.

- Complete the application and provide requested documentation.

- Allow for home appraisal to determine value.

Once the evaluation is complete, if approved, you'll receive the loan terms and subsequently access the funds to use as planned.

Using a Home Equity Loan Responsibly

Responsibly using a home equity loan is essential for maintaining financial stability. It's important to outline a clear plan for how you intend to use the loan funds before borrowing. By creating a budget and setting specific financial goals, you can help ensure that the funds are used effectively and contribute to your long-term financial well-being.

Moreover, borrowers should avoid using home equity loans for unnecessary or luxury spending. It's wise to prioritize spending that can increase the value of your home or improve your financial situation overall.

- Establish a clear budget and plan for use of loan funds.

- Avoid unnecessary or luxury expenditures.

- Consider using funds for home improvements or debt consolidation.

Implementing these practices will help you utilize a home equity loan responsibly, avoiding potential pitfalls associated with reckless borrowing.

Conclusion

In conclusion, home equity loans can be a highly beneficial financial tool for homeowners looking to access the value embedded in their property. They provide a pathway to liquidity for various needs while potentially offering tax benefits and lower interest rates.

However, the implications of borrowing against your home should not be taken lightly. Homeowners must weigh the advantages against the risks involved, meticulously evaluating their ability to repay.

By understanding the mechanics of home equity loans and maintaining responsible borrowing practices, homeowners can effectively leverage their equity while safeguarding their financial future.