Understanding credit scores is vital for anyone looking to apply for a loan or credit. A credit score provides a quick snapshot of an individual's creditworthiness based on their credit history and behaviors. Many factors influence this score, and even slight variations can swing your approval chances dramatically. In this blog post, we will explore what a credit score is, how it is calculated, and the significant role it plays in loan approvals.

We'll also look at strategies you can employ to improve your credit score and why lenders place such great importance on these numbers. Whether you’re planning to buy a home, a car, or any big-ticket item that requires financing, knowing about credit scores and how they impact loan approvals is crucial.

What is a Credit Score?

A credit score is a numerical representation of a person's creditworthiness based on their credit history. It typically ranges from 300 to 850, with higher scores indicating better credit. Lenders use credit scores to assess the risk of lending money or extending credit. There are several scoring models, but the most common ones include FICO and VantageScore.

Your credit score reflects your credit behavior, which includes timely payments, amounts owed, length of credit history, types of credit, and new credit inquiries. A strong score indicates reliability to potential lenders, while a poor score may challenge your chances of obtaining loans or might lead to higher interest rates.

How Credit Scores Are Calculated

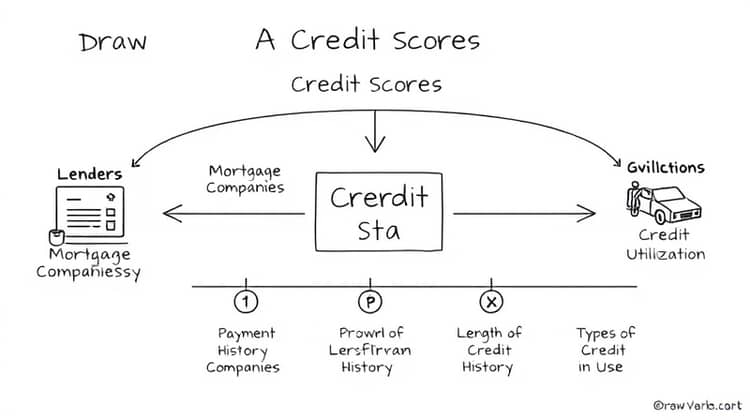

Credit scores are calculated using information provided in your credit report, which typically includes data from various sources like lenders, mortgage companies, and credit card companies. These reports track your payment history, total debts, credit utilization rates, and much more. The final credit score becomes a composite of these elements, determined by algorithms specific to the scoring model in use.

The primary components that contribute to your credit score include:

- Payment History (35%) - This is the most significant factor, highlighting whether you've made payments on time.

- Credit Utilization (30%) - This reflects the amount of credit you're using compared to your total available credit. Keeping this number low is favorable.

- Length of Credit History (15%) - A longer credit history can influence your score positively as it demonstrates your experience with managing credit.

- Types of Credit in Use (10%) - Having a mix of different types of credit (credit cards, loans, etc.) can be beneficial for your score.

- New Credit (10%) - Opening several new accounts within a short period can lower your score as it may indicate higher risk.

Understanding how these factors work together can empower you to make informed decisions that boost your credit health.

Why Do Lenders Care About Your Credit Score?

Lenders care about credit scores because it helps them assess the risk associated with lending money to an individual. A higher credit score generally signifies that a borrower is more trustworthy and likely to repay their debts. This risk assessment is crucial for lenders in determining whether they will approve a loan, the amount, and the interest rate.

Additionally, credit scores serve as a standardized measure that allows lenders to make quick decisions without the need for extensive background checks. A consistent method to evaluate creditworthiness can streamline the application process, making it easier for both the lenders and borrowers.

In many cases, lenders also consider credit scores as an early warning sign of potential financial distress. A drop in a credit score could signal to lenders that the borrower is experiencing financial difficulties, leading to cautious lending decisions.

How Credit Scores Impact Loan Approval

When you apply for a loan, your credit score often acts as a primary deciding factor in whether you will be approved or denied. Lenders have certain cutoff points for credit scores that dictate their lending decisions, meaning that if your score falls short, you may not even be considered for a loan.

- Creditworthiness: A higher credit score will increase your chances of loan approval.

- Interest Rates: A good credit score can result in lower interest rates, saving you money over the loan's lifespan.

- Loan Amounts: Lenders may be willing to extend larger amounts to borrowers with better credit histories.

Improving your credit score can open up financial opportunities, enabling you to secure loans more easily and at better terms.

Tips to Improve Your Credit Score

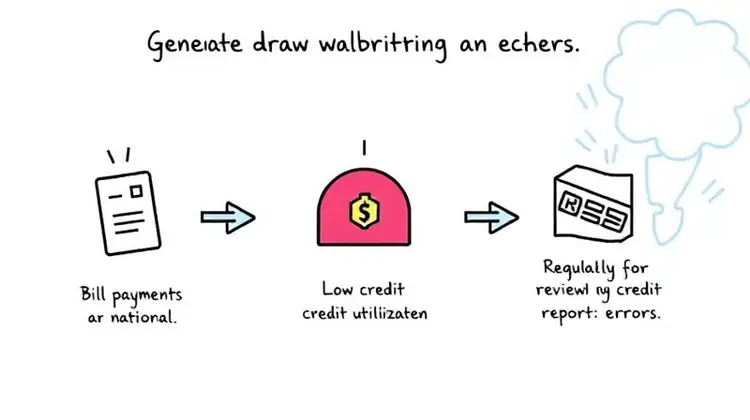

Improving your credit score is crucial for securing loans on favorable terms. Several strategies can help you bolster your standing over time. First, ensure that you consistently pay your bills on time; late payments can substantially hurt your score. Secondly, keep your credit utilization ratio below 30%, meaning you should ideally use only a fraction of your total available credit—this demonstrates fiscal responsibility.

Additionally, periodically reviewing your credit report for errors and disputing inaccurate information can also lead to score improvements. Challenge any negative items that shouldn't be there, as this exercise could boost your credit score significantly.

- Maintain on-time payments for all your debts.

- Limit credit inquiries and new accounts.

- Keep old accounts open to lengthen your credit history.

- Diversify your credit types as needed.

By being proactive in managing your credit, you put yourself in a better position to achieve your financial goals and secure loans when needed.

Conclusion

In summary, understanding and managing your credit score is essential for navigating the world of loans and credit. A good credit score can open doors to various financial opportunities, while a poor score can limit your options and lead to higher borrowing costs.

Taking the time to improve your credit score can pay off immensely in the long run. From securing more favorable loan terms to accessing higher amounts, having a robust credit score sets you up for success in future financial endeavors.