In today's financial landscape, securing a loan has become a common practice. However, borrowers often overlook one critical aspect: loan prepayment penalties. These penalties can impose financial burdens on those who wish to pay off their loans early. Understanding how to navigate around these penalties can save you significant amounts of money and help maintain your financial health.

This article will guide you through various strategies to avoid loan prepayment penalties, ensuring that you can manage your debt effectively without incurring unnecessary costs. Let's delve into each of these strategies to empower your borrowing experience.

1. Understand What Loan Prepayment Penalties Are

Loan prepayment penalties are fees that lenders may charge borrowers who pay off their loans early. These penalties are intended to protect the lender’s interest income, which they would lose if the loan is repaid before its term ends. The specifics of these penalties can vary by lender and the type of loan, which is why it's essential to understand the terms of your loan agreement.

For many borrowers, these penalties can come as a surprise, potentially costing thousands of dollars. Being aware of what these penalties are and how they might apply to your situation is the first step in avoiding them.

2. Read Your Loan Agreement Carefully

Your loan agreement is the most crucial document when it comes to understanding the terms and conditions of your loan. It contains important details about interest rates, payment schedules, and any potential penalties associated with paying off your loan early.

Take the time to read your loan agreement thoroughly. Look specifically for sections that mention prepayment penalties, as well as any stipulations regarding how much notice you must give prior to repaying your loan in full. Failing to understand these details could lead to unexpected expenses down the line.

- Identify whether your loan includes a prepayment penalty clause

- Understand how the penalty is calculated

- Check for any exceptions to the penalty provision

By being diligent in your review of the loan agreement, you can avoid costly surprises if you decide to pay off your loan ahead of schedule.

3. Ask About Prepayment Penalties Upfront

Before signing any loan agreement, always ask your lender directly about prepayment penalties. Some lenders are more flexible than others and may be willing to negotiate terms regarding these penalties. This proactive approach can help clarify any doubts you may have about the financial implications of your loan in advance.

When discussing with lenders, ensure you understand the types of loans they offer and how prepayment penalties work in each case. It's essential to have a clear understanding of the consequences of paying off a loan early, which can save you from financial setbacks in the future.

Additionally, keep in mind that not all loans come with prepayment penalties; being informed can empower you to make the best decisions.

4. Choose Loans Without Prepayment Penalties

If you want to ensure that you can pay off your loan without incurring extra charges, consider seeking out loans that do not include prepayment penalties. Many lenders, particularly credit unions and community banks, offer loans with more favorable terms that do not impose penalties.

Choosing a loan without prepayment penalties can provide you with the flexibility to manage your finances more effectively, allowing you to take advantage of opportunities like refinancing or paying off debt when it makes sense for your budget.

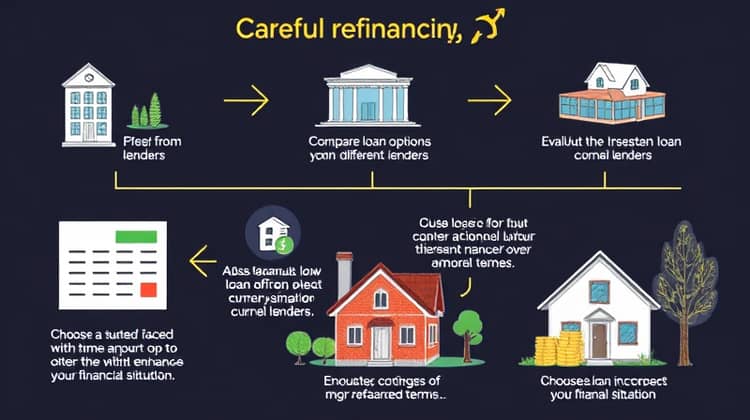

5. Refinance Carefully

Refinancing can be a great way to obtain better loan terms, but it’s crucial to do so cautiously to avoid getting locked into prepayment penalties again. When refinancing, assess your existing loan for any penalties and factor these into your decision-making process.

Don’t forget to compare various loan options from multiple lenders to find the best deal without prepayment penalties. By carefully choosing your refinanced loan, you can enhance your financial situation while minimizing potential costs.

- Obtain quotes from multiple lenders

- Choose a loan that fits your long-term financial goals

- Evaluate your current loan terms before making a decision

By taking your time to evaluate your refinancing options, you can secure a loan that suits your needs without unexpected penalties.

6. Consider Partial Payments

If you're looking to avoid penalties but still want to reduce your loan balance, consider making partial payments instead of full prepayments. Many lenders allow borrowers to pay more than the minimum amount due without penalties as long as the full loan is not paid off.

In this way, you can save on interest while still keeping your loan intact, thus avoiding prepayment penalties altogether.

- Check your loan agreement for rules on partial payments

- Discuss with your lender if they allow this option

- Make a plan to allocate extra funds towards your loan when possible

Partial payments can be a strategic way to manage your loan without incurring the hefty penalties associated with early repayment.

7. Plan for Penalties in Your Budget

When taking out a loan that includes prepayment penalties, it’s essential to account for these potential costs in your overall budget. Understanding the exact penalties involved can help you decide when might be appropriate to pay down your loan ahead of schedule, if at all.

Planning for any future penalties can also prevent you from being caught off guard should you decide to pay off your loan early.

- Set aside funds to cover potential penalties

- Reassess your budget periodically to account for changes in loans

- Evaluate the trade-off between paying off a loan early and the penalties incurred

By being financially prepared and strategic about your budget, you can manage any penalties effectively without unwanted stress.

8. Document All Payments

Maintaining detailed records of all payments made on your loan is essential. This documentation can assist in disputing any claims regarding prepayment penalties if needed, as well as providing clarity on your loan status as you approach the end of its term.

Make sure to keep receipts, bank statements, and any correspondence with your lender.

Doing so can help ensure your payments are accurately recorded and any potential issues regarding prepayment penalties are minimized.

- Keep all loan statements

- Store payment receipts in a secure place

- Document any adjustments made to your payment schedule

Being organized helps you stay on top of your payments, effectively reducing any chances of miscommunication with your lender.

9. Negotiating Payment Terms

If you find that a loan’s payment terms include prepayment penalties, don’t hesitate to negotiate these terms before finalizing your agreement. Many lenders are open to discussions about their loan offerings, especially if you demonstrate strong creditworthiness.

Being proactive in negotiations can lead to more favorable loan conditions and may allow you to secure a loan without prepayment penalties.

10. Seek Professional Advice

Consulting with a financial advisor or loan officer can provide valuable insights into managing loans with potential prepayment penalties. These professionals can help clarify complex terms and guide you in making informed decisions. Additionally, they can offer strategies specific to your financial situation that can keep you from falling into costly pitfalls.

Taking this step can provide peace of mind and ensure that you are fully aware of your options when it comes to loans and potential prepayment penalties.

Conclusion

Avoiding loan prepayment penalties is vital for managing your financial future. By being informed and proactive, you can take the necessary steps to ensure your borrowing experience remains manageable and cost-effective.

Remember to ask questions, read your agreements carefully, and seek the best loan options suited to your financial needs. Following these guidelines will help you navigate the world of loans successfully.