When taking out a loan, a loan agreement is one of the most crucial documents you'll encounter. It outlines the terms of the loan, the obligations of both parties, and ensures that everything is legally binding. Understanding how to read this document is essential to protecting your financial interests and ensuring that you are fully aware of your commitments.

However, for many, reading through such agreements can feel daunting and overwhelming. Loan agreements are often filled with legal jargon and complex terms that can obscure their meaning. This article will break down how to read a loan agreement effectively, equipping you with the knowledge you need to make informed decisions.

We'll explore key areas to focus on, provide a step-by-step guide to navigating these documents, and offer tips to help you better understand your loan agreement. By the end, you’ll have a clearer comprehension of your loan and be prepared to manage it responsibly.

Understand What a Loan Agreement Is

A loan agreement is a formal contract between a borrower and a lender. This document delineates the terms under which the lender provides money to the borrower, including the amount borrowed, interest rates, and repayment timelines. It serves as a legal framework governing the financial relationship between both parties.

Typically, a loan agreement covers various elements such as collateral, fees, and what happens if the borrower fails to make payments. This ensures both parties are on the same page regarding their rights and obligations. Understanding every clause in the loan agreement is critical; it can impact your financial health significantly over time.

Beyond simply being a contract, the loan agreement may also include provisions for dispute resolution, adjustments in payment schedules, and conditions under which the loan can be considered defaulted. Being informed about these terms helps borrowers navigate through potential pitfalls.

Key Terms to Look Out For

When reading a loan agreement, it is essential to pay attention to specific terminology that could significantly influence your responsibilities and the loan's overall cost.

- Principal Amount: The total sum of money that you borrow.

- Interest Rate: The percentage charged by the lender for borrowing the principal amount.

- Loan Term: The duration over which you have to repay the loan.

- Monthly Payment: The amount you need to pay each month until the loan is paid off.

- Default: The failure to repay the loan as per the terms set in the agreement.

Understanding these key terms is just the beginning. They form the core of your loan obligation and affect everything from your monthly budget to total interest paid over the life of the loan. Ensure you have clarity on each term before signing anything. Additionally, if anything is unclear, don't hesitate to ask the lender for clarification.

Failing to grasp these essential terms could lead to unintended financial consequences. Reading them carefully will empower you to manage your loan more effectively and confidently.

Step-by-Step Guide to Reading a Loan Agreement

To navigate through your loan agreement successfully, follow these steps for effective reading and comprehension.

- Read the entire document thoroughly without skipping any sections.

- Highlight key terms and phrases that stand out or raise concerns.

- Take notes on sections that require further clarification or explanation from the lender.

- Ask questions about anything you don't understand before signing the document.

- Review your notes and key terms once again to ensure you have grasped all aspects.

By following this structured approach, you can minimize confusion and enhance your understanding of the loan document. It gives you a methodical way to manage potentially overwhelming information and empowers you to make informed decisions about your financial future.

Tips for Reading Loan Agreements

Reading a loan agreement can be challenging, but a few practical tips can help simplify the process. Consider the following guidelines when approaching these documents:

Firstly, always take your time when breaking down the information. Don't rush through it; a hasty review can lead to mistakes and misunderstandings.

Secondly, be on the lookout for hidden fees or clauses buried in the fine print. Awareness of these charges can prevent unexpected costs later on.

- Use a dictionary or online resources to look up unfamiliar terms.

- Consider consulting with a financial advisor for guidance if necessary.

- Keep a separate document where you can collect your thoughts and any queries about the agreement.

Taking these tips into account will make the task less daunting and more manageable. Approaching your loan agreement with confidence and clear understanding will help you navigate your financial commitments more seamlessly.

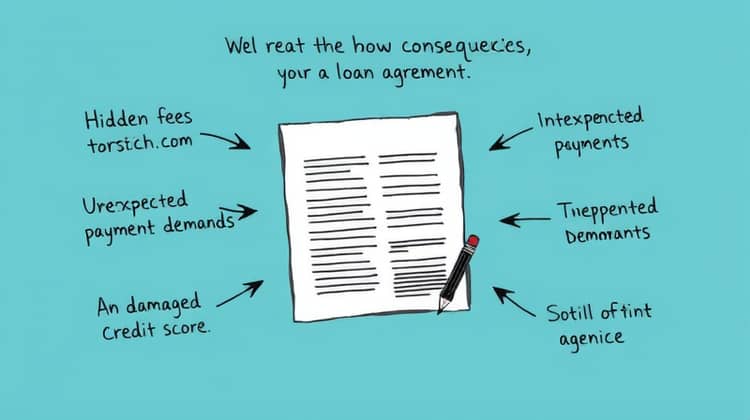

What Happens if You Don’t Read the Loan Agreement?

Failing to read and understand your loan agreement can lead to serious consequences. Ignorance of terms can result in incurring hidden fees, facing unexpected payment demands, or even falling into default. Once a loan is defaulted, it can have grave impacts on your credit score and future lending options.

Additionally, overlooking critical details can restrict your ability to negotiate changes in the loan terms. If you're not fully aware of your rights, you may miss out on opportunities that would better suit your financial situation.

Conclusion

In conclusion, understanding how to read a loan agreement is vital for any borrower. This knowledge will not only help you avoid pitfalls but also enable you to make informed financial decisions. By taking the time to read and comprehend the agreements, you can protect yourself from unpleasant surprises and consequences down the road.

Furthermore, if you find yourself overwhelmed by legal jargon, remember that resources are available. Financial advisors, family, or friends with experience can provide valuable insights and assistance. Don’t hesitate to seek help if needed, ensuring you fully understand what you are signing up for.

Ultimately, being proactive and informed about your loan agreement will empower you to borrow responsibly and maintain control over your financial future.