In today's world, student loan debt is an issue that affects millions of graduates each year. The burden of this debt can weigh heavily on young professionals as they try to establish their careers and maintain financial stability. Fortunately, there are strategies available that can help manage student loan debt and relieve some of the financial pressures.

Implementing these strategies can lead to a more proactive approach to handling student loans and may ultimately result in significant savings. The following six strategies will help you navigate the complexities of your student loans, choose the right repayment option, and work toward a brighter financial future.

1. Understand Your Loans

The first step in managing student loan debt is to understand the types of loans you hold and the total amount you owe. Familiarize yourself with the terms of your loans, interest rates, and repayment schedules. This information is crucial for making informed decisions about your debt.

Take the time to review your loan documents and use online resources to track your loan status. Knowledge is power when it comes to repayment options and potential benefits.

- Federal vs. private loans: Understand the differences and their implications for repayment.

- Interest rates can vary significantly, so know your rates to assess your total cost over time.

- Know your servicer: This is the company that manages your loans and can provide assistance if needed.

Understanding your loans allows you to create a well-informed strategy for repayment. By knowing how your loans work, you can identify the best options available to reduce financial strain.

2. Explore Repayment Plans

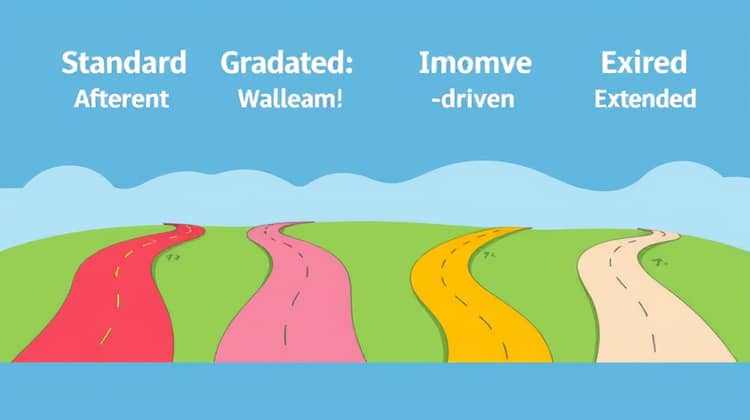

Once you have a clear understanding of your loans, it’s essential to explore the various repayment plans available. Federal student loans offer a variety of repayment options designed to fit different financial situations. Depending on your income and family size, you may qualify for plans that can significantly lower your monthly payments.

Take time to compare the different repayment plans, including the standard, graduated, income-driven, and extended repayment plans. Each has its pros and cons, so determine which works best for your unique circumstances.

- Standard Repayment Plan: Fixed payments over a 10-year period.

- Graduated Repayment Plan: Lower payments initially that increase every two years.

- Income-Driven Repayment Plans: Payments are based on your income and family size, making them more manageable.

- Extended Repayment Plan: Allows for longer repayment terms and lower monthly payments.

Choosing the right repayment plan can provide you with relief and stability in managing your student loan debt. Make sure to reassess your plan regularly as your financial situation changes to ensure it remains the best fit for you.

3. Consider Loan Forgiveness

Loan forgiveness programs can provide significant relief for qualifying borrowers. Programs like Public Service Loan Forgiveness (PSLF) aim to help those who dedicate their careers to public service, ensuring they are not burdened by their educational debt for life.

Research the eligibility requirements for loan forgiveness options. Depending on your profession, you may have opportunities to reduce or eliminate your student loan debt entirely.

- Public Service Loan Forgiveness (PSLF): Available for borrowers working in qualifying public service jobs.

- Teacher Loan Forgiveness: Available for teachers serving low-income schools.

- Income-Driven Repayment (IDR) forgiveness: Remaining balance forgiven after 20-25 years of payments.

If you qualify for a loan forgiveness program, it can be a game changer for your finances. Stay informed about these options and ensure you're on the right repayment plan to meet forgiveness requirements.

4. Refinance or Consolidate

Refinancing or consolidating your loans can be an effective way to manage student debt more efficiently. By refinancing, you can potentially secure a lower interest rate, which can lead to substantial savings over the life of your loan. Alternatively, consolidating your loans can simplify your payments by combining multiple loans into one.

Before deciding to refinance or consolidate, carefully evaluate your current financial situation, interest rates, and the terms of each loan to determine if it’s beneficial.

- Evaluate your current interest rates and payment terms.

- Research refinancing options with various lenders to find the best offer.

- Decide if consolidating is more suitable for your situation to simplify payments.

Remember that refinancing federal loans into private loans can lead to the loss of federal benefits, such as income-driven repayment plans or loan forgiveness. Weigh the pros and cons strategically to make an informed decision that fits your long-term financial goals. This option also allows you to take control of your student debt more effectively.

5. Budget and Prioritize

Creating a detailed budget can help you manage your finances effectively while navigating student loan repayment. Prioritizing your spending allows you to allocate funds directly toward your student loans and other essential expenses. By controlling your finances, you’ll be better positioned to make consistent payments on your loans.

Consider implementing strategies such as the 50/30/20 rule—where 50% of your income goes toward needs, 30% to wants, and 20% to savings and debt repayment. Adhering to a budget can significantly impact your ability to manage and pay off your student loans efficiently.

- Track all income and expenses to identify areas for saving.

- Allocate a set percentage of your income towards student loan payments each month.

- Regularly review your budget to make adjustments as needed.

A well-planned budget not only helps you make timely payments but also lessens stress and improves financial awareness. As you prioritize your debt, consider setting up automatic payments to ensure you never miss a due date, thus avoiding late fees and stress.

6. Seek Professional Advice

When feeling overwhelmed with student loan debt, don’t hesitate to seek professional help. Financial advisors or credit counselors can offer personalized advice tailored to your unique situation and help educate you on managing your loans better.

Research reputable organizations that specialize in student loan counseling. They can provide valuable information on repayment options, budgeting, and strategies for managing your overall financial health.

- Schedule a consultation with a financial advisor to discuss your options.

- Ask for referrals or recommendations for trusted student loan counseling agencies.

- Educate yourself about your loans: Utilize the resources recommended by professionals.

Professional advice can increase your understanding of complex financial situations and empower you to make better decisions regarding your loans. Remember, investing time in learning from experts today can pay off significantly in the future, paving the way to financial freedom.

Stay Informed and Proactive

Finally, staying informed about changes in student loan policies is crucial to effectively managing your debt. Legislative changes, interest rate fluctuations, and new repayment options can dramatically affect your repayment strategy and should not be overlooked.

Be proactive in seeking out educational resources, newsletters, podcasts, and seminars that focus on student loan management. Networking with other borrowers can provide valuable insights and experiences to learn from as you navigate your repayments.