When it comes to preparing for retirement, understanding the various investment options available is crucial. Two of the most common retirement savings plans are pension plans and 401(k) plans. Each has its unique features, benefits, and drawbacks, making it essential for individuals to comprehend their differences before deciding which is best for their retirement needs.

This article aims to shed light on both pension plans and 401(k) plans, detailing how they work, their advantages and disadvantages, and ultimately helping you assess which option may be more suitable for you.

What is a Pension Plan?

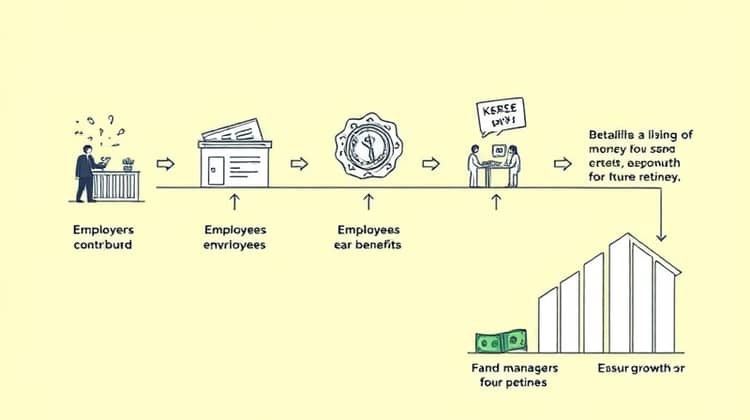

A pension plan is a type of retirement plan where an employer provides a specified sum of money to employees upon their retirement. These plans are designed to provide a steady income stream to retirees based on their salary and years of service. Unlike savings plans where individuals contribute from their salaries, pension plans are often funded entirely by the employer.

Pension plans fall under two main categories: defined benefit plans and defined contribution plans. Defined benefit plans guarantee a specific payout at retirement, while defined contribution plans depend on the contributions made by the employer and/or the employee, along with investment performance.

- Provides guaranteed income for retirees

- Less personal financial management required

- Usually funded by the employer

Pension plans represent a commitment by the employer to ensure financial security for employees after they retire. However, these plans have become less common in recent years, with many employers shifting towards more flexible options like 401(k) plans.

How Does a Pension Plan Work?

To begin with, pension plans work by requiring employers to make regular contributions towards a pool of funds that will eventually be used to pay retirees. The contributions can be based on a variety of factors, including employee salaries and years of service. Employees typically do not have to contribute directly to these plans as they might with a 401(k).

As employees work for the company, they earn benefits that increase with their years of service. Upon reaching retirement age, employees can access this pension fund, which pays a determined amount on a regular basis (monthly, quarterly, etc.).

Employers are responsible for managing pension fund investments to ensure that sufficient funds will be available when employees retire. This can include a mix of stocks, bonds, and other investment vehicles that are designed to grow the fund over time.

- Usually linked to job tenure

- Employees do not manage the investments

- Income is guaranteed for life

Pension plans require a significant commitment from employers and can lead to complexities in terms of management and funding, but they offer considerable benefits in terms of retirement security for employees.

Benefits of Pension Plans

Pension plans offer various advantages for employees, providing a sense of financial security upon retirement. One of the primary benefits is the guaranteed income for life, which alleviates the anxiety related to outliving one’s savings. Knowing that a steady stream of income will be available can greatly improve an individual’s quality of life in retirement.

Another significant benefit is that pension plans often require minimal management from the employee's side. The employer oversees the contributions and manages the investments, allowing retirees to enjoy their retirement without having to worry about their savings. This passive approach can be a significant relief for many individuals.

Additionally, pension plans can come with other financial perks, such as health insurance and cost-of-living adjustments, further enhancing the retirement experience for plan participants.

- Guaranteed income for life

- Less management responsibility for employees

- Potential for additional benefits

Overall, pension plans embody a safety net for individuals transitioning into retirement, ensuring that their financial needs are adequately met for years to come.

Drawbacks of Pension Plans

Despite the benefits, pension plans also have drawbacks. For instance, they are becoming increasingly rare as companies opt for more flexible retirement plans that require less long-term commitment. As a result, many employees may not have access to a pension plan at all, leaving them to rely on other savings forms.

Moreover, pension plans can be complex and may not cater to every individual's needs. Employees often cannot alter their benefits once they are set, potentially leading to insufficient funds if retirement occurs earlier than expected or if investment performance falters.

- May not be available to all employees

- Lack of flexibility regarding withdrawals

These considerations urge workers to diversify their retirement savings strategies rather than solely relying on pension plans.

What is a 401(k) Plan?

A 401(k) plan is a popular employer-sponsored retirement savings plan that allows employees to save a portion of their paycheck for retirement. Under this plan, employees can contribute their pre-tax earnings, which reduces their taxable income for the year. The contributions grow tax-deferred until withdrawal during retirement.

One of the distinctive features of a 401(k) is that employers often provide matching contributions, enhancing the amount employees can save. This feature incentivizes employees to invest in their retirement more than they might otherwise do, making it a beneficial tool for personal wealth building.

401(k) plans also offer employees a range of investment options to choose from, allowing participants to customize their portfolios according to their risk tolerance and retirement goals.

How Does a 401(k) Work?

In practice, employees decide how much of their salary to contribute to their 401(k) account, which is then deducted from their paycheck. Employers may match a percentage of these contributions up to a certain limit, effectively giving employees additional money towards their retirement savings. This matching contribution is often seen as 'free money' by the employees.

Employees have the discretion to choose how their funds are invested - options usually include mutual funds, stocks, or bonds, depending on the plan’s offerings.

- Tax-deferred growth

- Employer matching contributions

- Varied investment options

This model allows individuals to take greater control of their retirement finances compared to traditional pension plans.

Benefits of 401(k) Plans

One of the major benefits of a 401(k) plan is the tax advantages it provides. Since contributions are made pre-tax, employees can decrease their taxable income for the year, leading to lower tax bills.

Moreover, the potential for employer matching contributions makes a 401(k) especially attractive, maximizing employee savings without requiring additional personal investment. Many employers match contributions, which can encourage employees to contribute more towards their retirement.

Lastly, the flexibility of a 401(k) plan allows individuals to tailor their investment strategies so that they can align with their retirement goals and risk tolerance. This personalization assists employees in constructing a financial plan that meets their unique requirements.

- Tax advantages

- Employer match enhances savings

- Flexibility in investment choices

Drawbacks of 401(k) Plans

While 401(k) plans have many advantages, they also come with certain drawbacks. For one, there are usually limits on how much money an employee can contribute to their 401(k) each year, which may restrict how quickly an individual can save for retirement. Moreover, individuals may face penalties for withdrawing funds from their accounts before reaching retirement age, which discourages early access to their savings. This can be limiting for employees facing unexpected financial needs.

Additionally, the performance of a 401(k) plan heavily depends on the market conditions and the employee's investment choices, leading some individuals to experience less favorable outcomes than anticipated. The burden of investment decisions lies with the employee, which can be daunting for those who lack financial expertise.

- Contribution limits may hinder savings

- Withdrawal penalties

- Investment performance is not guaranteed

It is essential for employees to be well-educated on their options and to consider the implications of their investment decisions within a 401(k).

Key Differences Between Pension Plans and 401(k)

Pension plans and 401(k) accounts serve the same ultimate purpose of providing financial support during retirement, yet they do it in fundamentally different ways. The most notable difference is who is responsible for funding the retirement benefits. In pension plans, the employer typically shoulders the financial burden, providing a guaranteed income, whereas in a 401(k), the onus falls on the employee to contribute their own funds.

Another key difference is in the investment control. Employees participating in a pension plan generally do not have a say in how the funds are invested – the employer manages the investments. On the other hand, 401(k) plan participants enjoy the autonomy to choose their preferred investments, which can lead to a broader range of potential outcomes.

- Funding responsibility lies primarily with the employer in pension plans

- Employees contribute to their 401(k) plans

- Investment control varies markedly between the two options

Understanding these key differences can help individuals make informed choices about their retirement planning strategies.

Pension Plans vs. 401(k): Which is Better?

Deciding whether a pension plan or a 401(k) is better can significantly depend on an individual’s personal situation, financial requirements, and retirement goals. For those seeking guaranteed income and less management responsibility, a pension plan may be the ideal option. It can provide peace of mind knowing that a consistent income will be available throughout retirement.

Conversely, those who wish to have more control over their retirement savings may find a 401(k) more appealing. The ability to select investment options, combined with tax advantages and the prospect of employer matching contributions, makes a 401(k) plan a beneficial tool for wealth accumulation. Individual choice is a powerful aspect of the 401(k) structure, one many workers appreciate.

In summary, both plans have their strengths and weaknesses, and what works best for one individual might not be the case for another.

Ultimately, the best strategy may involve a combination of both pension plans and 401(k) approaches, leveraging the strengths of each to create a more comprehensive retirement strategy.

Conclusion

In conclusion, understanding the differences between pension plans and 401(k) plans is critical for anyone looking to secure their financial future. Each plan offers distinct advantages and potential drawbacks, and personal circumstances can dictate which option is more beneficial. It is essential for individuals to take account of their retirement goals, risk tolerance, and the level of involvement they wish to maintain in managing their retirement savings.

While pension plans may offer stability with their guaranteed income streams, 401(k) plans provide flexibility and control. Each employee must consider their personal financial situation and future goals to determine which plan aligns best with their needs. Educating oneself about the nuances effectively can significantly impact the success of one's retirement planning strategy.

Ultimately, whether one leans towards a pension or a 401(k), the critical aspect is to prioritize saving for retirement early and consistently to maximize financial security during one's golden years.