In the world of personal finance, the transition into retirement represents a pivotal moment. After years of diligent saving and investing, retirees are faced with the crucial task of ensuring their savings provide for their needs throughout retirement. This requires a clear understanding of withdrawal strategies that can help sustain their lifestyle while managing risks associated with market fluctuations and inflation.

Understanding how much to withdraw each year is as important as knowing how to save. With various strategies available, retirees must consider their financial situation, lifestyle goals, and potential additional income streams. The right plan allows retirees to enjoy their retirement years without the worry of outliving their savings.

In this article, we will explore several key withdrawal strategies—including the 4% rule, the bucketing strategy, and dynamic withdrawal strategies—to help you make informed choices about your retirement finances. Understanding these strategies will equip you with the knowledge needed to tailor a method that suits your unique circumstances.

Understanding the Basics

Before diving into specific strategies, it is essential to understand the fundamental principles of retirement withdrawals. Typically, retirees need to consider how long their retirement may last, their current expenses, and any potential income sources such as pensions or Social Security benefits.

Establishing a clear budget is also foundational to managing your retirement withdrawals. Knowing how much you spend and what essential expenses need to be covered will help guide your withdrawal decisions. This clarity assists in reducing anxiety around retirement spending.

Lastly, consider the investment vehicles you have used during your working years. Understanding how different accounts are taxed and how your portfolio will perform during retirement can influence the amount you decide to withdraw each year.

1. The 4% Rule

One of the most well-known retirement withdrawal strategies is the 4% rule. This principle posits that retirees can withdraw 4% of their savings annually with a high probability of not running out of money over a 30-year period.

The rule is grounded in historical market data and assumes a balanced portfolio of stocks and bonds. It offers a simple, standardized approach to deciding how much money to take out each year, aiming to ensure sustainability through various market conditions.

However, factors such as market performance, inflation, and changes in spending habits can influence the effectiveness of the 4% rule. Therefore, it is crucial to remain flexible in interpreting this guideline.

- The 4% rule provides an easy starting point for determining withdrawals.

- Market volatility may necessitate adjustments to the withdrawal percentage.

- This rule is based on historical performance and may not guarantee future results.

While the 4% rule offers a reliable framework, retirees should be aware of its limitations. Adjusting withdrawals in response to market conditions and personal needs can enhance financial longevity.

For example, if market conditions are favorable, it may allow for increased withdrawals without fear of outliving one’s savings, but in adverse conditions, like a market downturn, it may require reducing withdrawals to preserve capital.

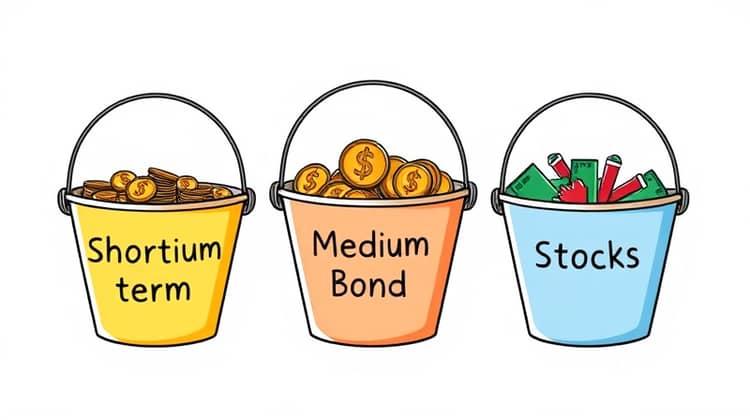

2. Bucketing Strategy

The bucketing strategy involves dividing retirement funds into several 'buckets' based on when the money will be needed. This strategy aims to mitigate risk by segregating assets into categories: short-term, medium-term, and long-term.

Typically, the first bucket covers immediate living expenses and is funded with low-risk investments, ensuring quick access to cash. The second bucket, for expenses in the mid-range future, can be invested in slightly riskier assets like bonds, while the long-term bucket can hold higher-risk investments such as stocks for growth.

This systematic approach focuses on meeting both short-term and long-term financial needs without the pressure of market fluctuations causing unplanned withdrawals.

- Create multiple buckets for different timeframes: immediate needs, intermediate needs, and long-term growth.

- Invest each bucket according to the timeframe—short-term in cash or certificates of deposit (CDs), medium-term in bonds, and long-term in equities.

- Review and adjust your buckets annually or as needs change to ensure optimal funding and growth.

This strategy also allows individuals to feel more secure, knowing that their immediate needs are buffered from the risks of market fluctuations. As market conditions change, retirees can dynamically adjust their strategies to optimize each bucket's performance.

Ultimately, the bucketing strategy helps retirees maintain a balance between risk and growth, ensuring a diverse approach to managing finances throughout retirement.

3. Dynamic Withdrawal Strategies

Dynamic withdrawal strategies are adaptive approaches to retirement spending. Unlike the fixed withdrawal amounts dictated by the 4% rule, dynamic strategies allow flexibility based on portfolio performance and individual circumstances.

These strategies often involve withdrawing a percentage of the portfolio’s value at the beginning of each year, adjusting the amount based on investment performance. This means if the portfolio grows, the withdrawals can increase; conversely, if the portfolio decreases, withdrawals can be reduced to preserve capital.

Dynamic withdrawals align closely with market performance and can help adjust to changing needs without a rigid structure that may not fit.”

- Withdrawals can be based on a percentage of portfolio value each year.

- Adjust plans according to market performance, inflation, and lifestyle changes.

- This approach requires continuous monitoring and may have higher levels of planning complexities.

These strategies can enhance sustainability and longevity of funds by scaling withdrawals up or down based on financial conditions. Nevertheless, they require discipline and ongoing evaluation.

Retirees must also consider their ability to adapt lifestyle changes to align with market performance, thereby decreasing the stress related to financial volatility.

4. RMD (Required Minimum Distributions)

Required Minimum Distributions (RMD) are crucial for individuals with tax-advantaged accounts like IRAs and 401(k)s. Starting at age 72, the IRS requires retirees to withdraw a minimum amount from these accounts each year, irrespective of their actual needs.

Understanding RMD rules is critical, as failure to withdraw the required minimum can result in steep penalties. Essentially, the government mandates this to ensure tax compliance and collect revenues on tax-deferred accounts rather than allowing the wealth to pass indefinitely without taxation.

Planning for RMDs ahead of time can help retirees incorporate these mandatory withdrawals into their yearly income planning, minimizing potential tax impacts and aligning with overall retirement income strategies.

Tax Considerations

Taxes can significantly impact retirement withdrawals. Investors should aim to strategize withdrawals that minimize their tax liabilities in retirement while maximizing take-home income.

This often involves a mix of taxable accounts, tax-deferred savings, and tax-free withdrawals. Planning when and how to withdraw from these accounts can greatly affect one’s overall tax burden in retirement.

Mixing and Matching Strategies

No single strategy might perfectly fit all retirees; often a combination of methods tailored to individual circumstances yields the best outcomes. Retirement planning necessitates evaluating multiple factors, including personal risk tolerance, expenses, and changes in life situations.

Economically prudent retirees frequently blend strategies like the 4% rule with dynamic withdrawals or the bucketing approach to create a more resilient withdrawal plan that adapts to their unique financial landscape.

Getting Professional Help

Many retirees may benefit from professional guidance in developing a solid withdrawal strategy. Financial advisors can offer personalized advice based on an individual's financial situation, retirement goals, and market conditions.

Additionally, professionals can help retirees understand tax implications and maintain a diversified portfolio that will effectively support their income needs throughout retirement.

- Seek out a fiduciary advisor who is committed to putting your best interests first.

- Discuss your long-term goals, expenses, and concerns to create a tailored withdrawal strategy.

- Review your plan regularly with your advisor to adjust as necessary based on new financial needs or changing market conditions.

Investing in professional guidance can lead to better financial outcomes, ultimately ensuring retirees can enjoy their desired lifestyle with peace of mind.

Conclusion

Navigating retirement withdrawal strategies is essential for ensuring a sustainable income throughout retirement years. As shown, various approaches exist that can be tailored to fit individual financial situations and lifestyles.

From the 4% rule to dynamic withdrawal methods, understanding these strategies allows retirees to make informed choices regarding their financial futures. Furthermore, integrating tax considerations into planning can minimize tax liabilities, thus enhancing spending power during retirement.

Ultimately, seeking professional assistance can be beneficial in navigating the complexities of retirement finances and ensuring a secure, enjoyable retirement.