Understanding credit card grace periods is essential for anyone looking to manage their finances effectively. These grace periods can play a significant role in reducing interest charges and improving cash flow. Knowing how they work can help consumers make informed decisions about their credit card usage and payments.

In this article, we will explore the concept of grace periods, how they function, their importance in financial management, and strategies for consumers to make the most out of them. We'll also cover some of the limitations, such as when grace periods do not apply, to give you a fully rounded understanding.

What is a Grace Period?

A grace period is a designated time frame provided by credit card issuers during which cardholders can pay their outstanding balance without incurring interest charges. Essentially, this is an interest-free period that encourages responsible borrowing and timely payments.

Typically, grace periods start the day after your billing cycle ends and last until the payment due date. For a borrower to take advantage of the grace period, they must pay their full balance within this timeframe.

How Does a Credit Card Grace Period Work?

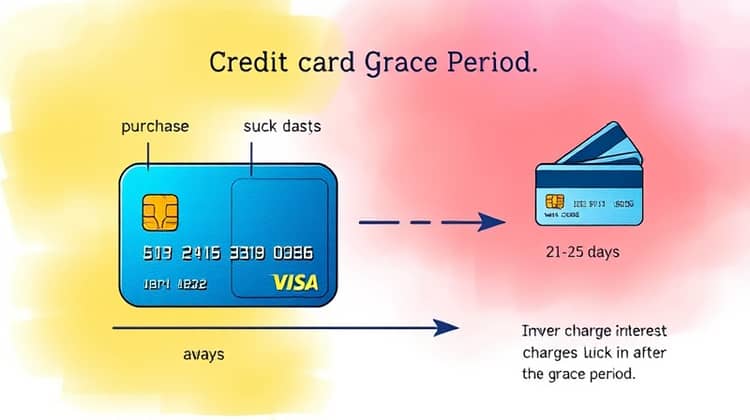

The grace period primarily applies to new purchases made with the credit card. If you pay off your full balance by the due date, you typically won’t incur any interest charges on those purchases.

- Grace periods usually last between 21 to 25 days.

- They apply only if you have paid your previous balance in full and on time.

- After the grace period ends, any unpaid balances will start accruing interest immediately.

- New purchases made during the billing cycle can benefit from the subsequent grace period if paid off.

Understanding how this mechanism operates is crucial for effective credit card management. By leveraging the grace period, consumers can avoid unnecessary interest charges and keep their credit costs down.

It's also worth noting that grace periods can vary significantly between different credit card issuers and types of credit cards, so it’s essential to read the fine print of your card's agreement.

Importance of the Grace Period

The grace period holds immense importance for both consumers and credit providers. For cardholders, it represents an opportunity to manage cash flow effectively; by allowing time for payments without penalty, consumers can better align their spending with income.

Furthermore, the grace period incentivizes responsible credit use. It encourages individuals to pay their balances in full rather than merely making minimum payments, which can lead to crippling debt over time.

No Grace Period: Cash Advances and Balance Transfers

While grace periods provide a significant advantage for new purchases, they do not apply to cash advances or balance transfers. If you use your credit card to withdraw cash or transfer a balance from another account, interest begins accruing immediately—often at a higher rate than for regular purchases.

This lack of grace period on such transactions means that borrowers should tread carefully. Cash advances can often lead to high-interest debt if not managed properly, and balance transfers can add complexity to your repayment strategy due to differing interest rates.

Therefore, it's prudent to avoid cash advances unless absolutely necessary and to understand the terms and conditions surrounding any balance transfers to mitigate financial risks.

Strategies to Maximize the Grace Period

To maximize the benefits of the grace period, consider establishing a routine of paying off your full credit card balance before the due date each month. This allows you to take full advantage of the interest-free time frame on purchases made.

Setting up automatic payments or reminders can help ensure that you never miss a due date, thereby maintaining your grace period eligibility. Additionally, try to make purchases that fit comfortably within your budget, making it easier to pay off your balance swiftly.

It's also wise to review and understand your credit card statement thoroughly. Many statements will outline when your grace period ends and what transactions may take place during it, which can help you plan better.

Lastly, consider using a credit card that offers an extended grace period as one of its features. Some cards cater specifically to users looking for more manageable payment terms.

Changes in Grace Period Policies

Like many financial products, credit card companies may revise their policies regarding grace periods in response to changes in economic conditions or regulatory requirements.

- Some issuers may shorten the grace period duration in their terms.

- Others may introduce new fee structures that can affect how grace periods function.

- Watch for promotional offers that extend grace periods temporarily.

Keeping abreast of these changes can protect consumers from unexpected charges or loss of benefits, ensuring they remain savvy with their credit management.

Conclusion

In conclusion, understanding credit card grace periods is a vital component of effective financial management. They can save consumers significant amounts of money in interest if used properly. By taking advantage of these periods, borrowers can cultivate good financial habits that support their long-term financial health.

As the landscape of credit card policies evolves, staying informed about the grace periods and any changes to them can help consumers make better decisions, ensuring their credit usage is both advantageous and sustainable.